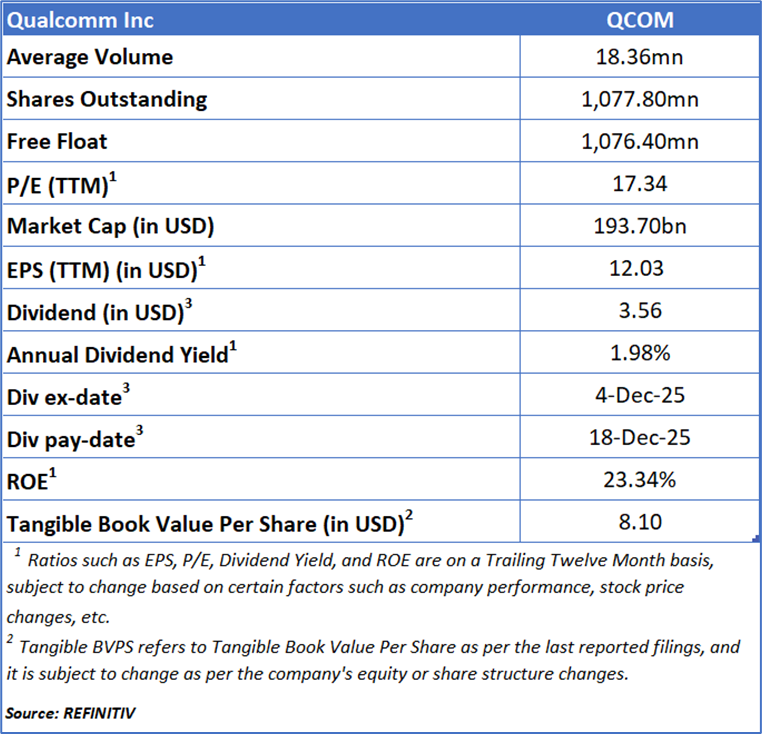

Qualcomm Incorporated

Qualcomm Incorporation (NASDAQ: QCOM) designs, develops, and commercializes core technologies that power the global wireless communications industry. The company’s innovations span 3G, 4G, and 5G connectivity, as well as high-performance, energy-efficient computing and on-device artificial intelligence solutions. Qualcomm operates through three primary segments: Qualcomm CDMA Technologies (QCT), which focuses on semiconductor products; Qualcomm Technology Licensing (QTL), which manages its extensive patent portfolio; and Qualcomm Strategic Initiatives (QSI), which handles strategic investments and related activities.

As per previous Kalkine’s Earnings Hunter Report published on ‘QCOM’ on Jun 27, 2025, Kalkine provided an ‘Attractive’ stance on the stock at USD 158.51 based on fundamental analysis and the stock price has now moved up by ~ 13.38% since then.

Noted below are the details of support and resistance levels provided in our previous report:

Rationale:

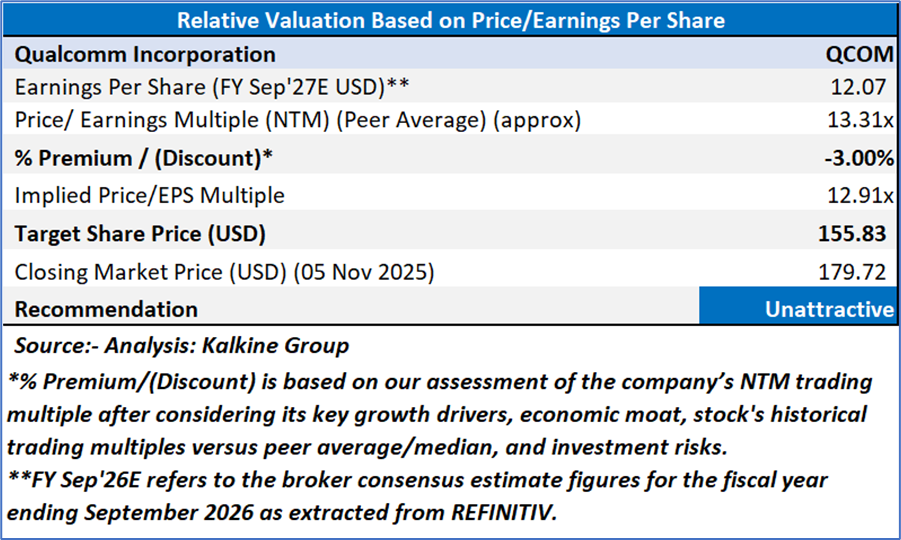

Valuation (Using Price/Earnings per share Multiple)

Share Price Chart

Conclusion

Qualcomm’s FY2025 results, while strong on a Non-GAAP basis, reveal several underlying weaknesses that temper its growth outlook. The company recorded a significant GAAP net loss due to a USD 5.7 billion non-cash tax charge, exposing vulnerability to shifting U.S. tax legislation. Its licensing segment (QTL) continued to weaken, reflecting declining revenues and profitability amid intensifying legal and competitive pressures. Meanwhile, rising operating expenses from acquisitions, share-based compensation, and R&D spending have begun to weigh on margins. Compounding these issues, Qualcomm remains highly dependent on a few large customers and the Chinese market, making it susceptible to geopolitical risks and industry cyclicality, which could constrain long-term stability and valuation expansion.

Based on the notional gains, valuation downside and price action stance, a "Unattractive" recommendation on Qualcomm Incorporation (NASDAQ: QCOM) has been given at the closing market price of USD 179.72 as on 05 November 2025.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is 05 November 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level which the stock is expected to reach as per the relative valuation method and/or technical analysis taking into consideration both short-term and long-term scenario.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the London Stock Exchange (LSE) and or REFINITIV. Typically, both sources (LSE and or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.’

Note 6: Dividend Yield may vary as per the stock price movement.

Kalkine Equities LLC, with Delaware File Number 4697384, Foreign Qualification Registration in California File Number 202109211078, and Texas File Number 805521396, is authorized to provide general advice only. The information on https://kalkine.com/ does not take into account any of your investment objectives, financial situation or needs. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions. The link to our Terms and Conditions and Privacy Policy has been provided for your reference. On the date of publishing the reports (mentioned on the website), employees and/or associates of Kalkine do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations later.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...