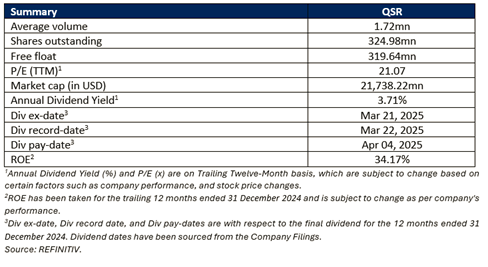

Restaurant Brands International Inc

Restaurant Brands International Inc (NYSE: QSR) is a fast-food restaurant company that owns and franchises quick-service dining establishments. It specializes in serving coffee, beverages, and a variety of food items. The company operates through several segments, including Tim Hortons (TH), Burger King (BK), Popeyes Louisiana Kitchen (PLK), Firehouse Subs (FHS), International (INTL), and Restaurant Holdings.

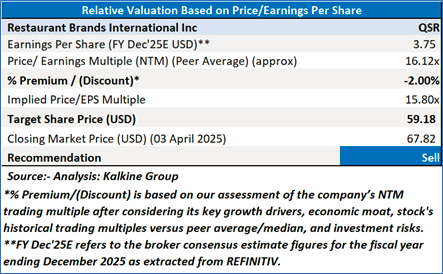

Recommendation Rationale – SELL at USD 67.82

QSR’s Daily Price Chart

Valuation Methodology: Price/Earnings Approach

QSR faced multiple challenges in 2024, with sluggish system-wide sales growth across key brands, particularly Burger King and Firehouse Subs. Adverse foreign exchange movements further weakened financial results, while rising operating expenses, especially in advertising and G&A costs, pressured profitability. The Restaurant Holdings segment underperformed, with Carrols Burger King and Popeyes China struggling due to operational disruptions. Strategic initiatives, like Burger King’s "Reclaim the Flame," have yet to show meaningful impact, and slowing restaurant growth raises concerns about QSR’s long-term expansion strategy. Persistent headwinds suggest ongoing difficulties in maintaining momentum and profitability.

Given its current trading levels, downside indicated by valuation, and risks associated, it is prudent to book profit at the current levels. Hence, a ‘Sell’ recommendation is given on the stock at the closing price of USD 67.82, as of April 03,2025.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and geopolitical issues prevailing geopolitical tensions. Therefore, it is prudent to follow a cautious approach while investing.

Note 1: Past performance is neither an indicator nor a guarantee of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance levels is April 03,2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Kalkine Equities LLC, with Delaware File Number 4697384, Foreign Qualification Registration in California File Number 202109211078, and Texas File Number 805521396, is authorized to provide general advice only. The information on https://kalkine.com/ does not take into account any of your investment objectives, financial situation or needs. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions. The link to our Terms and Conditions and Privacy Policy has been provided for your reference. On the date of publishing the reports (mentioned on the website), employees and/or associates of Kalkine do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations later.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...