Investment Rationale:

Investing in new S&P 500 entrants provides a unique opportunity as their inclusion forces institutional buying and boosts liquidity, often leading to immediate price appreciation. These companies, which meet stringent financial criteria, tend to signal robust profitability and growth potential. Additionally, heightened investor interest and increased analyst coverage can lead to a short-term performance advantage and pave the way for continued expansion and earnings growth over the long term.

This report provides the coverage on 2 new entrants to S&P500; TKO Group and Williams-Sonoma

TKO Group Holdings, Inc. (NYSE: TKO)

TKO Group Holdings, Inc. (NYSE: TKO) is a sports and entertainment company specializing in combat sports and related events. It owns several major properties, including the Ultimate Fighting Championship (UFC), a leading mixed martial arts organization; World Wrestling Entertainment, Inc. (WWE), which focuses on sports entertainment; and Professional Bull Riders (PBR), an organization dedicated to bull riding competitions.

Recent Business and Financial Updates

Technical Observation (on the daily chart):

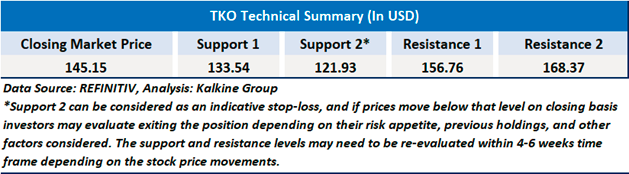

The stock is experiencing a pullback, trading below the 21-day moving average and approaching the 50-day moving average (~USD 153), a key support level. RSI is near 36, indicating weakening momentum but not yet oversold. Recent volume spikes suggest strong selling pressure. If the stock holds above USD 153, a rebound is possible, but a breakdown below this level could lead to further downside. Resistance is around USD 160, aligning with the 21-day MA.

TKO Group Holdings, Inc. achieved record financial performance in 2024, driven by strong growth at both UFC and WWE. The company reported USD 2.804 billion in revenue and USD 1.251 billion in Adjusted EBITDA, reflecting increased sponsorships, live event revenues, and strategic cost reductions. Despite legal settlements impacting net income, TKO remains financially robust with strong cash flow generation. Looking ahead, the company targets up to USD 3.0 billion in revenue for 2025, fueled by new media rights agreements, expanded live events, and continued business integration. With a clear strategic focus, TKO is well-positioned for sustained growth and shareholder value creation.

As per the above-mentioned price action, recent key business and financial updates, momentum in the stock over the last month, and technical indicators analysis, a ‘Buy’ rating has been given to TKO Group Holdings, Inc. (NYSE: TKO) at the closing market price of USD 145.15 as of March 11,2025.

Williams-Sonoma, Inc. (NYSE: WSM)

Williams-Sonoma, Inc. (NYSE: WSM) is a multi-channel specialty retailer specializing in home products. Its portfolio includes brands like Williams Sonoma, Pottery Barn, Pottery Barn Kids, Pottery Barn Teen, West Elm, Williams Sonoma Home, Rejuvenation, and Mark and Graham. These brands are promoted and sold through e-commerce platforms, direct-mail catalogs, and physical retail stores.

Recent Business and Financial Updates

Technical Observation (on the daily chart):

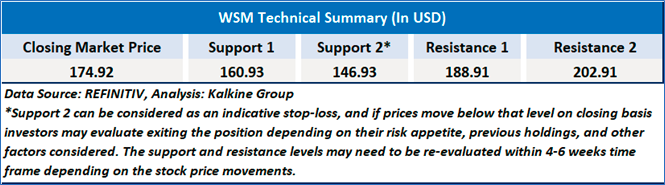

Williams-Sonoma (WSM) remains in a long-term uptrend but is currently pulling back, trading just below its 50-day moving average (~200.45). Support is near 190, while resistance is in the 200-205 range. The RSI at 44.52 suggests neutral to slightly oversold conditions. A breakout above 205 could resume the uptrend, while failure to hold 190 may lead to further downside. Volume remains moderate, indicating no major selling pressure yet.

WSM delivered strong third-quarter results, exceeding revenue and profit expectations, driven by improved sales trends, market share gains, and robust profitability. Despite a 2.9% decline in comparable brand revenue, the company achieved a 17.8% operating margin and a 7.1% increase in EPS to USD 1.96, supported by expanded gross margins and supply chain efficiencies. Strong liquidity enabled USD 606 million in shareholder returns, and a new USD 1 billion stock repurchase authorization further underscores confidence in future performance. With a raised fiscal 2024 guidance, improved operational efficiency, and long-term growth expectations, Williams-Sonoma continues to demonstrate resilience and strategic strength in a challenging market.

As per the above-mentioned price action, recent key business and financial updates, momentum in the stock over the last month, and technical indicators analysis, a ‘Buy’ rating has been given to Williams-Sonoma, Inc. (NYSE: WSM) at the closing market price of USD 174.92 as of March 11,2025.

Individuals can evaluate the stock based on the support and resistance levels provided in the report in case of keen interest taking into consideration the risk-reward scenario.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and prevailing geopolitical tensions. Therefore, it is prudent to follow a cautious approach while investing.

Related Risk: This report may be looked at from a high-risk perspective and a recommendation is provided for a short duration. This report is solely based on technical parameters, and the fundamental performance of the stocks has not been considered in the decision-making process. Other factors which could impact the stock prices include market risks, regulatory risks, interest rates risks, currency risks, social and political instability risks etc.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is March 11,2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level that the stock is expected to reach as per the relative valuation method and or technical analysis taking into consideration both short-term and long-term scenarios.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the New York Stock Exchange (NYSE), NASDAQ Capital Markets (NASDAQ), and or REFINITIV. Typically, all sources (NYSE, NASDAQ, or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.

Kalkine Equities LLC, with Delaware File Number 4697384, Foreign Qualification Registration in California File Number 202109211078, and Texas File Number 805521396, is authorized to provide general advice only. The information on https://kalkine.com/ does not take into account any of your investment objectives, financial situation or needs. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions. The link to our Terms and Conditions and Privacy Policy has been provided for your reference. On the date of publishing the reports (mentioned on the website), employees and/or associates of Kalkine do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations later.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...