Netflix, Inc

Netflix, Inc (NASDAQ: NFLX) operates as an entertainment platform that develops, licenses, and acquires content, including its own original programming. The Company offers subscription-based access in more than 190 countries, providing audiences with a wide range of TV series, movies, and games across multiple genres and languages.

Recent Business Developments:

Netflix is set to acquire Warner Bros. for a total consideration of about USD 82 billion including debt, marking a shift from its traditional strategy of growing through internal development rather than major acquisitions. In what resembles a high-stakes competitive process, Netflix outbid Paramount Skydance, Comcast, and other potential buyers to secure the Warner Bros. streaming and studio businesses owned by Warner Bros. Discovery.

As a result of the transaction, Netflix becomes the largest entertainment company globally with a market capitalisation exceeding USD 400 billion, further consolidating its industry influence. The company will pay USD 82.7 billion via a mix of cash and stock, implying an equity valuation of around USD 72 billion. According to co-CEO Greg Peters, the acquisition is expected to significantly enhance Netflix’s content offering and support long-term business acceleration.

The deal materially strengthens Netflix’s strategic positioning, scale, and intellectual property depth, shifting it from a dominant streaming platform to a vertically integrated entertainment superpower. However, the transaction is expensive and execution-heavy, implying a period of heightened integration risk and financial pressure. In summary, the acquisition is transformational and strategically logical, but its ultimate success hinges on Netflix’s ability to integrate and monetize premium assets while sustaining disciplined capital allocation.

Key Growth Aspects

Growth Challenges

Technical Observation (on the daily chart):

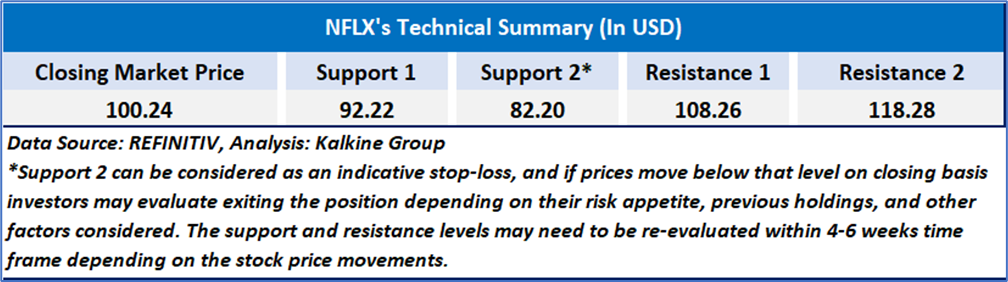

Netflix’s share price appears to have shifted into a downtrend after peaking around mid-year, with a series of lower highs and lower lows since September. The price is now trading below both the 50-day and 20-day moving averages, which are also sloping lower, reinforcing bearish momentum, while the recent breakdown below USD 105 shows renewed selling pressure. The RSI has slipped toward oversold territory (around 28), suggesting the stock may be short-term stretched to the downside, but confirmation of any rebound would require a sustained move back above the short-term moving averages and an improvement in volume trends.

Netflix delivered strong year-on-year revenue growth and healthy free cash flow in Q3 2025, supported by robust engagement and an expanding advertising business; however, profitability was dampened by a sizable one-off Brazilian tax expense, which pushed operating margin below guidance. While the company continues to benefit from global content success and rising share of TV view time, management also acknowledged an increasingly competitive entertainment landscape and the need for sustained investment in content and technology to maintain momentum.

As per the above-mentioned price action, recent key business and financial updates, momentum in the stock over the last month, and technical indicators analysis, a ‘Watch’ rating has been given Netflix, Inc (NASDAQ: NFLX) at the closing market price of USD 100.24 as of Dec 05,2025.

Individuals can evaluate the stock based on the support and resistance levels provided in the report in case of keen interest taking into consideration the risk-reward scenario.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and prevailing geopolitical tensions. Therefore, it is prudent to follow a cautious approach while investing.

Related Risk: This report may be looked at from a high-risk perspective and a recommendation is provided for a short duration. This report is solely based on technical parameters, and the fundamental performance of the stocks has not been considered in the decision-making process. Other factors which could impact the stock prices include market risks, regulatory risks, interest rates risks, currency risks, social and political instability risks etc.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is December 05,2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level that the stock is expected to reach as per the relative valuation method and or technical analysis taking into consideration both short-term and long-term scenarios.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the New York Stock Exchange (NYSE), NASDAQ Capital Markets (NASDAQ), and or REFINITIV. Typically, all sources (NYSE, NASDAQ, or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.

Kalkine Equities LLC, with Delaware File Number 4697384, Foreign Qualification Registration in California File Number 202109211078, and Texas File Number 805521396, is authorized to provide general advice only. The information on https://kalkine.com/ does not take into account any of your investment objectives, financial situation or needs. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions. The link to our Terms and Conditions and Privacy Policy has been provided for your reference. On the date of publishing the reports (mentioned on the website), employees and/or associates of Kalkine do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations later.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...