The Walt Disney Company

The Walt Disney Company (NYSE: DIS) is a diversified worldwide entertainment company. The Company's segments include Entertainment, Sports and Experiences.

Key Business and Financial Updates:

- Overall Financial Performance: The Walt Disney Company reported fiscal 2025 revenues of USD 94.4 billion, a 3% increase year over year, with fourth-quarter revenue broadly flat at USD 22.5 billion versus the prior-year period. Income before income taxes more than doubled to USD 12.0 billion for the year and rose to USD 2.0 billion in Q4, while total segment operating income expanded 12% annually to USD 17.6 billion despite a 5% decline in Q4 to USD 3.5 billion. Full-year diluted EPS increased sharply to USD 6.85 from USD 2.72, and adjusted EPS rose 19% to USD 5.93, although Q4 adjusted EPS declined modestly by 3% to USD 1.11.

- Segment Results: Entertainment, Sports, and Experiences: In the Entertainment segment, full-year operating income increased 19% to USD 4.7 billion, supported by growth in Direct-to-Consumer and Content Sales/Licensing, while Q4 operating income declined to USD 691 million due to tough theatrical comparisons and lower Linear Networks performance, including the deconsolidation of Star India. Sports delivered Q4 operating income of USD 911 million, down 2% year over year, as higher domestic ESPN marketing and rights costs offset advertising and subscription revenue gains, though full-year Sports operating income rose 20% to USD 2.9 billion. Experience remained the key profit engine, with record full-year operating income of USD 10.0 billion and record Q4 operating income of USD 1.9 billion, driven by 6% revenue growth and robust contributions from both Domestic and International Parks & Experiences as well as Consumer Products.

- Direct-to-Consumer and Subscriber Metrics: Disney’s Direct-to-Consumer business continued to improve profitability, with Q4 DTC revenue rising 8% to USD 6.2 billion and operating income increasing 39% to USD 352 million, reflecting higher effective pricing and subscriber growth, partially offset by elevated programming, technology, and marketing costs. At quarter-end, Disney+ subscriptions reached 131.6 million (up 3% sequentially), while Hulu totaled 64.1 million subscribers (up 15% sequentially), with blended Disney+ ARPU improving modestly and Hulu ARPU mixed due to subscriber mix shifts and lower advertising revenue in certain tiers. Linear Network revenues and operating income declined, reflecting lower advertising and affiliate revenues, reduced political advertising, and the impact of the Star India transaction, while Content Sales/Licensing and Other posted weaker Q4 results owing to the extraordinarily strong prior-year theatrical slate (Inside Out 2, Deadpool & Wolverine) versus a more moderate current slate.

- Guidance, Capital Allocation, and Shareholder Returns: For fiscal 2026, Disney guides to double-digit adjusted EPS growth, underpinned by double-digit operating income growth in Entertainment (weighted to the second half), low-single-digit growth in Sports, and high-single-digit growth in Experiences. Management plans approximately USD 24 billion of content investment across Entertainment and Sports, USD 9 billion in capital expenditures, and expects around USD 19 billion in operating cash flow, while incurring pre-opening and dry-dock costs tied to Disney Cruise Line expansion, particularly Disney Adventure and Disney Destiny. The Company has doubled its share repurchase target to USD 7 billion for fiscal 2026 and declared a cash dividend of USD 1.50 per share, payable in two installments of USD 0.75 in January and July 2026, thereby reinforcing its commitment to returning capital to shareholders alongside continued growth investment.

- Strategic Positioning, Cash Flow, and CEO Commentary: Disney generated USD 18.1 billion in operating cash flow in fiscal 2025, up 30% year over year, and USD 10.1 billion in free cash flow, aided by improved Experiences profitability, lower Entertainment content spend following the Star India transaction, and tax-payment deferrals related to California disaster relief. Capital expenditure increased to USD 8.0 billion, primarily reflecting higher investment in cruise ship fleet expansion and new park attractions. CEO Robert A. Iger emphasized that fiscal 2025 marked another year of strategic progress, highlighting the strengthening of the direct-to-consumer portfolio, the resilience of Parks & Experiences, and the benefits of Disney’s diversified business model and balance sheet in supporting high-quality content and enhanced shareholder returns.

Key Risks

- Dependence on Content Performance and Linear Network Weakness: Disney remains exposed to fluctuations in content success and the ongoing decline of traditional TV, where softer advertising, shrinking subscriber bases, and variable theatrical performance can weigh on profitability across key Entertainment units.

- Execution Challenges in Direct-to-Consumer Profitability: The Company’s strategic shift toward streaming requires disciplined management of content spending, pricing, and subscriber retention, and heightened competition increases the risk that revenue growth may not keep pace with rising operating and technology costs.

- High Capital Requirements and Sensitivity in Parks & Experiences: Disney’s large-scale investments in cruise ships, park expansions, and new attractions elevate financial and operational risk, while performance in its Experiences segment remains highly sensitive to macroeconomic conditions and discretionary travel trends.

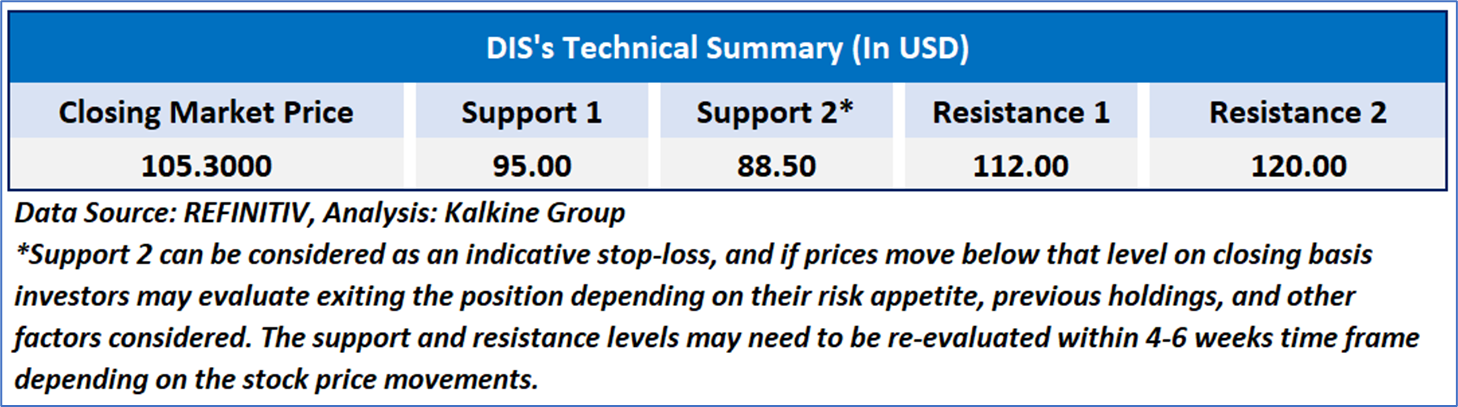

Technical Observation (on the daily chart):

- Price Structure and Moving Averages: DIS has remained in a downward-leaning trend since late summer, with the stock now trading near USD 105 and positioned below both the 21-day and 50-day moving averages, which continue to slope downward—indicating that the intermediate bias remains weak despite prior recovery attempts earlier in the year.

- Momentum and RSI Behaviour: The RSI at around 44 reflects muted momentum and a slight bearish tilt, showing that selling pressure has eased but no clear reversal signal has emerged. While momentum improved during mid-year gains, it has since settled into a neutral-to-soft range.

- Volume Patterns and Market Participation: Volume has remained consistent with brief surges during volatility, but recent trading shows moderate participation as the stock consolidates. A meaningful increase in volume, coupled with a move back above key moving averages, would be necessary to suggest a more constructive technical shift.

The Walt Disney Company (NYSE: DIS) delivered steady fiscal 2025 performance with full-year revenue rising 3% to USD 94.4 billion and income before taxes more than doubling, supported by strong gains in segment operating income and substantial EPS expansion. Entertainment, Sports, and Experiences contributed differently across the year, with Experiences generating record profits, DTC showing improving profitability alongside subscriber growth at Disney+ and Hulu, while Linear Networks and theatrical results faced tougher comparisons. Management issued positive fiscal 2026 guidance, highlighting double-digit adjusted EPS growth, significant content and capital investment, and increased shareholder returns through higher buybacks and dividends. Operational cash flow and free cash flow strengthened meaningfully, supported by cost efficiencies and improving performance across key businesses. Technically, the stock remains under pressure, trading below major moving averages with subdued momentum, though consolidation persists while market participants await clearer signals of trend recovery.

As per the above-mentioned price action, important resistance near USD 105-USD 115, momentum in the stock over the last month, and technical indicators analysis, a ‘WATCH’ rating has been given for The Walt Disney Company (NYSE: DIS) at the closing price of USD 105.30, as of December 05, 2025.

Individuals can evaluate the stock based on the support and resistance levels provided in the report in case of keen interest taking into consideration the risk-reward scenario.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and prevailing geopolitical tensions. Therefore, it is prudent to follow a cautious approach while investing.

Related Risk: This report may be looked at from a high-risk perspective, and a recommendation is provided for a short duration. This report is solely based on technical parameters, and the fundamental performance of the stocks has not been considered in the decision-making process. Other factors which could impact the stock prices include market risks, regulatory risks, interest rates risks, currency risks, social and political instability risks etc.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance level is December 05, 2025. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Target Price refers to a price level that the stock is expected to reach as per the relative valuation method and or technical analysis taking into consideration both short-term and long-term scenarios.

Note 5: ‘Kalkine reports are prepared based on the stock prices captured either from the New York Stock Exchange (NYSE), NASDAQ Capital Markets (NASDAQ), and or REFINITIV. Typically, all sources (NYSE, NASDAQ, or REFINITIV) may reflect stock prices with a delay which could be a lag of 15-20 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.

Please wait processing your request...

Please wait processing your request...