Key Highlights

- Century-Long Dividend Legacy — General Mills has paid dividends continuously for over 125 years, currently offering a historically high 7.07% yield ($0.61/quarter, $2.44 annualized) — the highest GIS yield in many years, driven by a near-40% stock price decline from its 52-week high.

- Recession-Proof Brand Portfolio — With iconic household names like Cheerios, Haagen-Dazs, Betty Crocker, and Blue Buffalo spanning breakfast, snacks, ice cream, and premium pet food, General Mills generates over $2 billion in annual free cash flow that comfortably covers its dividend obligations.

- Deep Value at a Steep Discount — Trading at a P/E of just 8.42x — among the lowest in the S&P 500 consumer staples sector — GIS presents a compelling contrarian opportunity as volume trends stabilize and the premium pet food segment continues its structural growth.

In an era of economic uncertainty and persistent inflation, consumer staples companies occupy a unique investment position: their products are purchased by consumers regardless of economic conditions, providing earnings stability that underpins reliable dividend payments. General Mills, Inc. (NYSE:GIS) — the maker of Cheerios, Haagen-Dazs, Betty Crocker, and dozens of other beloved brands — currently offers income investors an attractive dividend yield of approximately 7.07%, making it one of the highest-yielding consumer staples names in the S&P 500. This analysis explores the full investment case for GIS.

Company Overview

Founded in 1856 and headquartered in Golden Valley, Minnesota, General Mills is one of the world's largest food companies. The company operates across four reportable segments: North America Retail, International, Pet, and North America Foodservice. Its brand portfolio is extraordinarily diverse, spanning breakfast cereals, snacks, baking products, ice cream, yogurt, and premium pet food brands including Blue Buffalo.

General Mills serves consumers in more than 100 countries and generates annual net sales of approximately $19–20 billion. The company has strategically evolved its portfolio over the past decade, divesting lower-growth businesses and acquiring higher-growth natural and organic brands, as well as expanding meaningfully into the pet food category through the 2018 acquisition of Blue Buffalo — a transaction that has proven highly successful.

The pet food business deserves special mention: pet ownership surged during the pandemic, and Blue Buffalo has maintained strong market share in the premium pet food category, providing General Mills with a higher-growth revenue stream that complements its mature core food business.

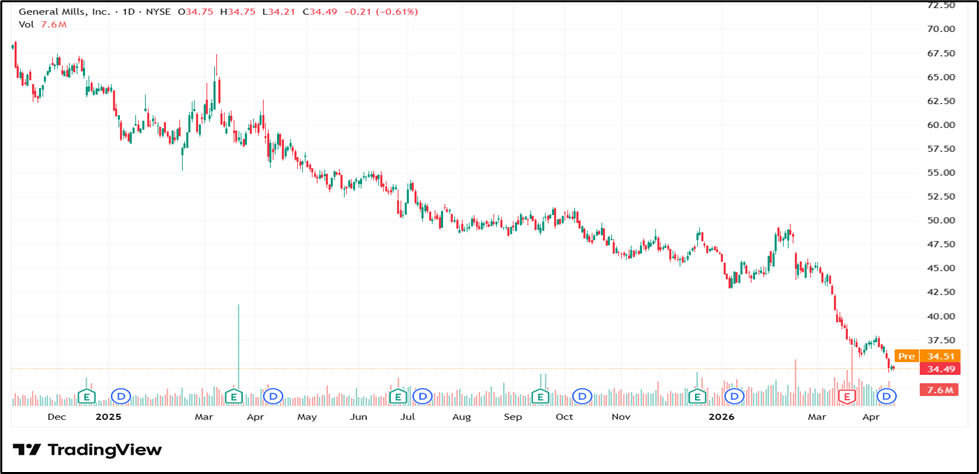

Stock Performance — April 2026

General Mills shares closed at $34.49 on April 15, 2026, down 0.61% (−$0.21) on the day. The stock recovered slightly in after-hours trading, adding +$0.060 (+0.17%) to reach $34.55. The session opened at $34.75, touched a high of $34.75, and fell to a low of $34.20.

|

Price (Apr 15, 2026) $34.49 |

Daily Change −0.61% / −$0.21 |

After Hours $34.55 |

|

Open $34.75 |

Day High $34.75 |

Day Low $34.20 |

|

52-Week High $58.47 |

52-Week Low $34.04 |

Market Cap $1.84KCr |

|

P/E Ratio 8.42 |

Dividend Yield 7.07% |

Quarterly Div. $0.61 |

The stock's 52-week range of $34.04 to $58.47 reveals a dramatic de-rating over the past year — General Mills shares have fallen nearly 40% from their 52-week high, driven by concerns about volume weakness, private label competition, and slowing organic sales growth. At a P/E of just 8.42x, the stock is priced at a significant discount to historical averages and consumer staples peers. For income investors, the 7.07% yield at current levels is the highest GIS has offered in many years.

Financial Overview

General Mills has faced a challenging consumer environment in fiscal 2025–2026, as elevated food prices have driven some consumers toward private label alternatives and reduced purchase frequency in certain categories. Organic net sales growth has decelerated meaningfully from pandemic-era highs, and volume declines have partially offset pricing gains.

Despite these pressures, General Mills has maintained solid operating margins through cost efficiency programs and supply chain optimization. The company generates strong free cash flow — typically in excess of $2 billion annually — which more than covers its dividend obligations. The dividend payout ratio, while elevated relative to recent earnings trends, remains comfortably funded by free cash flow.

The P/E ratio of 8.42x is among the lowest for any S&P 500 consumer staples company, reflecting significant pessimism about near-term volume trends. Many value investors view this discount as a potential opportunity given the company's brand portfolio strength and long-term earnings power.

Dividend History and Analysis

General Mills has paid dividends continuously for well over a century — one of the longest uninterrupted dividend payment records in U.S. corporate history. The current quarterly dividend of $0.61 per share equates to an annualized payout of $2.44. At the current stock price of $34.49, this represents a yield of approximately 7.07%.

GIS has grown its dividend consistently, though the pace of growth has moderated in recent years as management balances dividend growth with debt reduction following the Blue Buffalo acquisition. The dividend payout ratio based on free cash flow remains healthy, providing confidence in dividend sustainability even in a weaker earnings environment.

The current 7.07% yield is notably higher than GIS's historical average yield of 3–4%, largely reflecting the significant stock price decline rather than an increase in the dividend itself — a pattern that has historically rewarded patient income investors who have purchased at similar yield levels.

Management Outlook and Guidance

General Mills CEO Jeff Harmening has guided the company through a challenging period with a focus on brand investment, innovation, and cost discipline. For fiscal year 2026 (ending May 2026), management has guided toward a return to modest organic net sales growth as volume trends stabilize and pricing remains supportive.

Key strategic priorities include pet food growth (Blue Buffalo), accelerating in snacking through the Snack Bars and Haagen-Dazs segments, and driving efficiency through the company's Accelerate strategy. Management has signaled an intention to maintain the dividend while prioritizing debt reduction and organic investment.

_05_20_2026_22_15_04_838839.png)

_05_20_2026_15_03_17_853649.png)

Please wait processing your request...

Please wait processing your request...