Self-employed Americans can choose between IRA, Roth IRA, SEP IRA and Solo 401(k) plans. Learn how each works in 2026 and how to structure retirement contributions efficiently.

Key Highlights

- Solo 401(k) plans offer the highest contribution capacity for self-employed individuals in 2026.

- IRAs and Roth IRAs provide lower limits but remain useful for tax Diversification and flexibility.

- Many self-employed professionals combine multiple retirement accounts to optimise tax outcomes.

Self-employment offers income flexibility but removes access to employer-sponsored retirement plans. As a result, individuals must independently structure retirement savings using IRS-approved accounts.

The main Options include Traditional IRAs, Roth IRAs, SEP IRAs, SIMPLE IRAs and Solo 401(k) plans. Each differs in contribution capacity, tax treatment and administrative complexity. Choosing between them is less about a single “best” option and more about how they interact within an overall retirement strategy.

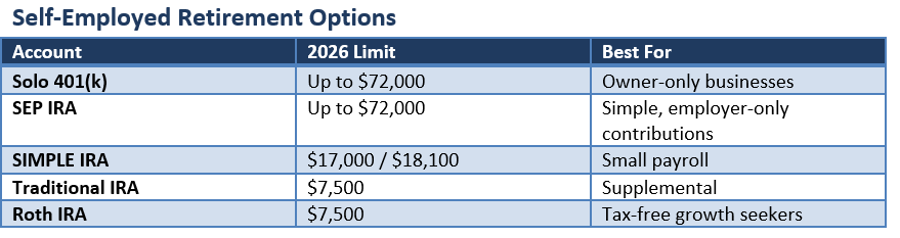

Solo 401(k): High Contribution Capacity for Owner-Only Businesses

The Solo 401(k) is often the most powerful retirement structure available to self-employed individuals with no employees other than a spouse.

For 2026, total combined contributions can reach approximately $72,000, depending on income and plan design, making it the highest ceiling among mainstream retirement accounts.

A key feature is flexibility in tax treatment. Contributions can be made on a pre-tax basis or, in many plans, as Roth deferrals. Unlike Roth IRAs, Roth Solo 401(k) contributions are not subject to income limits, expanding access for higher earners.

However, the structure comes with administrative requirements. Once Assets exceed certain thresholds, filings such as Form 5500-EZ may be required.

Traditional IRA: Simplicity with Limited Capacity

The Traditional IRA remains a foundational retirement tool due to its simplicity and broad accessibility.

For 2026, individuals can contribute up to $7,500 annually, subject to eligibility rules and potential deduction phase-outs if they or their spouse participate in a workplace retirement plan.

The key advantage is tax-deferred growth, while the limitation is relatively low contribution capacity compared with employer-style plans.

Roth IRA: Tax-Free Growth with Income Limits

The Roth IRA provides tax-free qualified withdrawals in retirement, funded by after-tax contributions.

Like the Traditional IRA, the annual limit for 2026 is $7,500. However, eligibility phases out at higher income levels, limiting access for some self-employed professionals with strong Earnings growth.

Despite the constraints, Roth IRAs remain valuable for long-term tax diversification, especially when combined with pre-tax accounts.

SEP IRA: High Limits with Employer Contributions Only

The SEP IRA is designed for simplicity and high contribution flexibility, particularly for freelancers and small Business owners.

Contributions are made solely by the employer and can reach up to 25 percent of compensation, subject to annual IRS limits that align broadly with other retirement caps.

While easy to administer, SEP IRAs lack employee deferral features and may offer less tax flexibility compared with Solo 401(k) plans.

SIMPLE IRA: Lower Limits, Easier Administration

The SIMPLE IRA is generally used by small businesses with employees.

In 2026, employee deferrals are capped at around $17,000, with additional catch-up contributions available for older participants.

While less powerful in terms of contribution size, it offers easier setup and lower administrative complexity compared with more advanced retirement structures.

Combining Accounts: A Common Strategy

Many self-employed individuals do not rely on a single account type.

A common structure includes:

- Solo 401(k) for maximum contribution capacity

- Roth IRA for tax-free retirement diversification

- Taxable brokerage accounts for Liquidity and additional savings flexibility

This layered approach helps balance tax efficiency, access to Capital, and long-term Wealth accumulation.

Choosing the Right Structure

The optimal retirement setup depends on three core factors:

- Income level and Volatility

- Business structure and whether employees exist

- Tax strategy preferences between pre-tax and Roth contributions

High earners often prioritise Solo 401(k) plans for scale, while early-stage freelancers may rely on IRAs before upgrading to more advanced structures.

Conclusion

Self-employed Americans operate in one of the most flexible Retirement Planning environments in the U.S. tax system. No single account dominates in all situations. Instead, the best outcomes typically arise from combining multiple structures to balance tax treatment, contribution capacity and liquidity.

The Solo 401(k) stands out for scale, while IRAs and Roth IRAs provide essential diversification tools. SEP and SIMPLE IRAs remain relevant for specific business contexts where simplicity is prioritised.

A structured, multi-account approach often delivers the most resilient retirement framework for self-employed individuals.

Please wait processing your request...

Please wait processing your request...