Traditional IRA contributions may reduce Taxable Income in 2026, but deduction limits depend on income and workplace retirement plan coverage. Here's what taxpayers need to know.

Key Highlights

- Traditional IRA contributions may be fully, partially, or not deductible depending on income and retirement plan participation.

- Workplace retirement plan coverage triggers income-based deduction phase-outs.

- Nondeductible IRA contributions remain available and must be tracked using IRS Form 8606.

The traditional IRA remains one of the few retirement accounts that can provide an immediate tax benefit through deductible contributions. However, not every taxpayer qualifies for the full deduction. The IRS applies income limits and workplace retirement plan rules that can reduce or eliminate deductibility.

Understanding how these rules work can help taxpayers evaluate whether a traditional IRA offers a current-year tax advantage and how it fits within a broader Retirement Planning strategy.

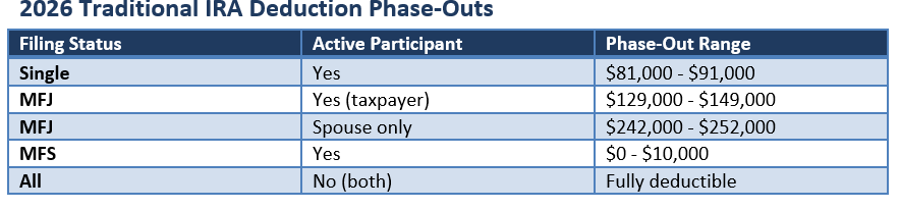

When Traditional IRA Contributions Are Fully Deductible

The most favorable tax treatment generally applies when neither the taxpayer nor a spouse is covered by an employer-sponsored retirement plan.

In this situation, eligible taxpayers can typically deduct the full amount of their traditional IRA contribution, up to the annual IRS contribution limit. For 2026, the IRA contribution limit is $7,500, with an additional $1,100 catch-up contribution available for individuals aged 50 and older.

Because no income phase-out applies when neither spouse participates in a workplace plan, deductibility is generally straightforward.

How Workplace Retirement Plans Affect Deductibility

The rules become more complex when the taxpayer participates in a workplace retirement plan such as a 401(k), 403(b), pension, or similar employer-sponsored arrangement.

For 2026, the IRS applies deduction phase-outs based on modified adjusted gross income (MAGI):

- Single filers covered by a workplace plan: $81,000 to $91,000.

- Married filing jointly with the contributing spouse covered: $129,000 to $149,000.

- Married filing separately: generally $0 to $10,000.

As income moves through these ranges, the available deduction gradually declines until it is eliminated.

Special Rules for Spouses

A different set of income limits applies when the IRA contributor is not covered by a workplace retirement plan but their spouse is.

For married couples filing jointly, the deduction begins to phase out between $242,000 and $252,000 of modified adjusted gross income in 2026.

This provision allows many non-covered spouses to claim at least a partial deduction even when the other spouse participates in an employer-sponsored retirement plan.

Nondeductible Contributions Still Have Value

Losing the deduction does not necessarily mean losing access to a traditional IRA.

Taxpayers may still make nondeductible contributions up to the annual contribution limit, provided they meet eligibility requirements. These contributions continue to benefit from tax-deferred growth inside the account.

However, investors must properly track nondeductible contributions using IRS Form 8606. Failure to maintain accurate records can create tax complications when distributions are taken later.

Understanding the Backdoor Roth Strategy

Nondeductible traditional IRA contributions are often discussed in connection with the so-called backdoor Roth strategy.

This approach involves making a nondeductible contribution to a traditional IRA and subsequently converting those funds to a Roth IRA. While the strategy remains permissible under current law, investors should understand the pro-rata rule, which can affect the taxable portion of a conversion when other pre-tax IRA Assets exist.

Because tax outcomes can vary significantly, careful planning is important before executing a conversion.

Why Annual Reviews Matter

IRA deduction limits and income thresholds are periodically adjusted for Inflation. Taxpayers who qualified for a deduction one year may find their eligibility changes the next due to higher income, workplace plan participation, or revised IRS limits.

Reviewing contribution eligibility before year-end can help avoid surprises at tax filing time and ensure retirement contributions are structured efficiently.

Conclusion

The traditional IRA Tax deduction remains a valuable retirement planning tool, but eligibility depends heavily on income and workplace retirement plan coverage. While some taxpayers qualify for a full deduction, others may receive only a partial benefit or none at all.

Even when contributions are not deductible, traditional IRAs can still provide tax-deferred growth opportunities. Understanding deduction phase-outs, tracking nondeductible contributions correctly, and reviewing eligibility annually can help taxpayers make more informed retirement planning decisions.

Please wait processing your request...

Please wait processing your request...