Key Highlights

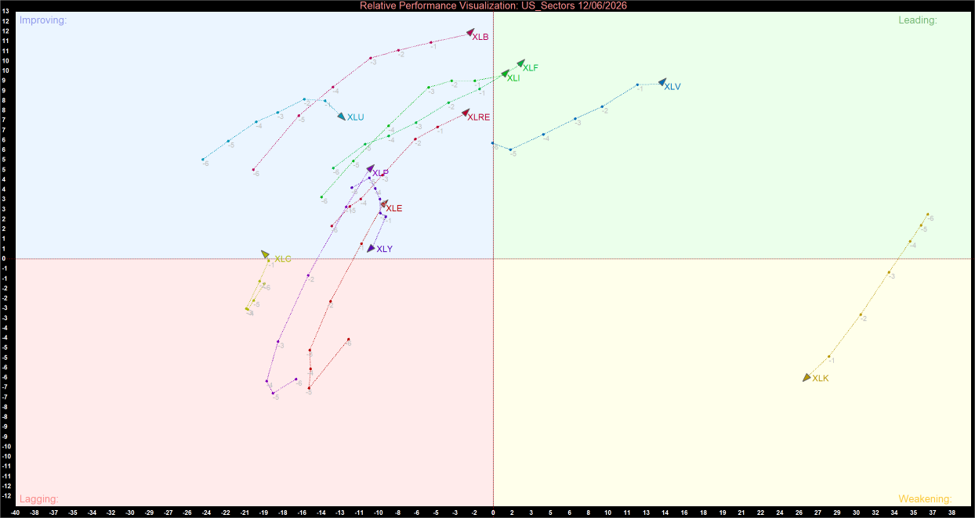

- No Sectors Remain in Lagging: The most notable development is the complete absence of sectors in the Lagging quadrant, highlighting broad participation and improving market breadth.

- Financials and Industrials Maintain Leadership: Financials (XLF) and Industrials (XLI) remain firmly positioned in the Leading quadrant, signaling continued institutional confidence in economically sensitive sectors.

- Health Care Continues to Lead: Health Care (XLV) remains one of the strongest momentum leaders, combining positive relative strength with robust momentum.

- Materials Exhibits Strongest Momentum: Materials (XLB) remains in the Improving quadrant but displays the highest momentum reading on the chart, positioning the sector as a potential future leader.

The US sector rotation profile remained highly constructive on June 12, 2026, with leadership broadening across multiple sectors and no areas of the market exhibiting significant relative weakness. The latest Relative Rotation Graph (RRG) shows a healthy distribution of sectors between the Leading and Improving quadrants, reflecting strong institutional participation across both cyclical and defensive industries.

Unlike narrow rallies driven by a handful of sectors, the current structure suggests investors are allocating capital across a wide range of opportunities, creating a more balanced and sustainable market environment.

US Sector Momentum Summary

US Sector Relative Momentum Chart (at the closing price of 12/06/2026). Powered by: amibroker.com

Key Market Themes

Leadership Remains Broad and Balanced

Health Care (XLV), Financials (XLF), and Industrials (XLI) continue to occupy the Leading quadrant. The presence of both defensive and cyclical sectors among market leaders reflects a balanced investment environment rather than a narrowly concentrated rally.

Materials Approaches Leadership

Materials (XLB) exhibits the strongest momentum reading on the chart and sits just outside the Leading quadrant. The sector's trajectory suggests continued institutional accumulation and increasing confidence in commodity-linked industries.

Improving Quadrant Dominates the Landscape

Seven sectors currently reside in the Improving quadrant, including Real Estate (XLRE), Utilities (XLU), Consumer Staples (XLP), Energy (XLE), Consumer Discretionary (XLY), and Communication Services (XLC). This concentration indicates that relative momentum is strengthening across a broad range of industries.

Technology Remains Strong Despite Weakening Momentum

Technology (XLK) is the sole sector in the Weakening quadrant. However, it remains far to the right of the benchmark, indicating exceptionally strong relative strength. While momentum has cooled, the sector continues to be an important source of market leadership.

Absence of Lagging Sectors Signals Healthy Breadth

The lack of any sectors in the Lagging quadrant is perhaps the most bullish feature of the current RRG structure. It suggests that institutional capital is broadly supporting the market rather than concentrating in a small number of sectors.

Bottom Line

The June 12 sector rotation profile presents one of the healthiest market structures seen in recent months. Financials (XLF), Industrials (XLI), and Health Care (XLV) continue to lead, while Materials (XLB) exhibits the strongest momentum and appears poised to challenge for leadership.

Meanwhile, seven sectors occupy the Improving quadrant and no sectors remain in Lagging, highlighting exceptionally broad market participation. Although Technology (XLK) remains in Weakening, its strong relative-strength position suggests the sector continues to provide important support to the broader market.

Overall, the current RRG configuration points to a constructive and well-balanced market environment, with sector rotation supporting the potential for a more sustainable advance across US equities.

_06_12_2026_23_00_13_327450.jpg)

Please wait processing your request...

Please wait processing your request...