Key Highlights

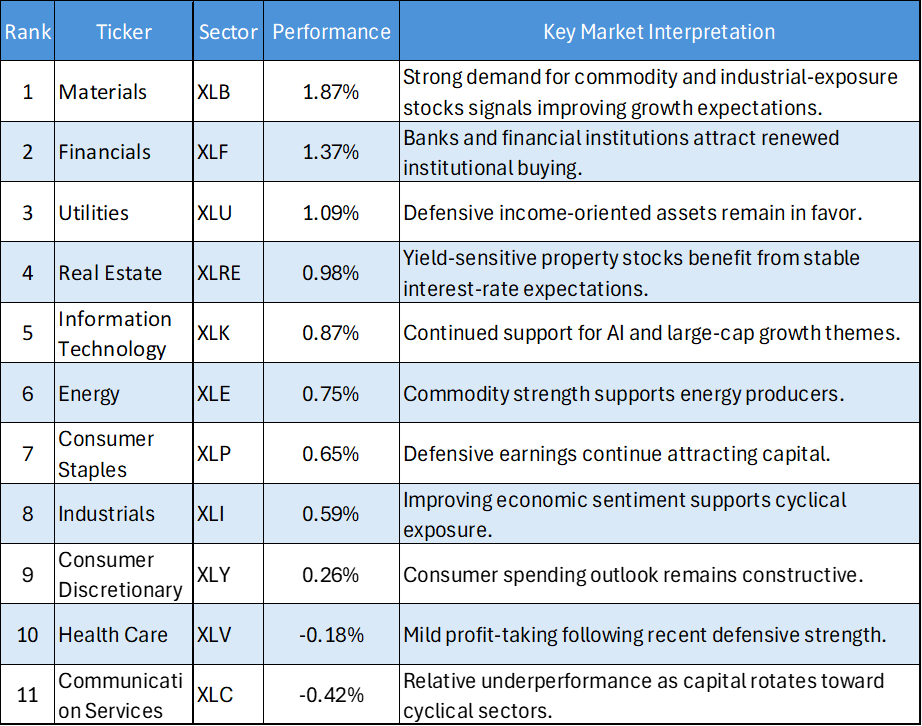

- Materials Emerges as Market Leader: Materials (XLB) surged 1.87%, delivering the strongest sector performance of the session as investors increased exposure to commodity-linked equities amid improving economic sentiment and expectations for continued industrial demand.

- Financials Rebound Strongly: Financials (XLF) advanced 1.37%, marking one of the most significant improvements among major sectors. The rally suggests renewed institutional confidence in banks and diversified financial companies following recent periods of consolidation.

- Defensive Sectors Continue Participating: Utilities (XLU) gained 1.09%, while Real Estate (XLRE) rose 0.98% and Consumer Staples (XLP) added 0.65%. The simultaneous strength across defensive sectors indicates investors remain focused on portfolio stability despite increasing risk appetite.

- Only Two Sectors Finish Lower: Health Care (XLV) declined 0.18% and Communication Services (XLC) fell 0.42%, highlighting the broad-based nature of the market advance as nine of eleven major sectors closed in positive territory.

The US equity market session on June 12, 2026, demonstrated a healthy and broadly diversified advance across sectors. Unlike recent sessions characterized by sharp rotations between growth and defensive positioning, investors displayed a willingness to allocate capital across multiple segments of the market simultaneously.

The breadth of participation suggests institutional investors are becoming increasingly constructive on the near-term economic outlook. Cyclical sectors such as Materials and Financials led gains, while traditionally defensive groups including Utilities, Real Estate, and Consumer Staples also attracted meaningful inflows. This combination reflects a balanced risk environment rather than an aggressive speculative rally.

Daily US Sector Performance Summary

Key Market Themes

Materials Assumes Leadership

- The defining development of the session was the strong outperformance of Materials (XLB), which climbed 1.87% to lead all major sectors. The advance reflects growing institutional confidence in economically sensitive industries tied to construction, manufacturing, and commodity demand.

- Unlike previous rallies dominated by a narrow group of technology stocks, the strength in Materials suggests investors are increasingly willing to position for broader economic expansion. The sector's leadership may also indicate expectations for continued infrastructure spending and resilient industrial activity.

Financials Reclaim Investor Attention

- Financials (XLF) delivered one of the strongest performances of the day, gaining 1.37%. The move is particularly important given the sector's influence on broader market direction.

- Banks and financial institutions often serve as indicators of investor confidence in economic growth. The strong participation from Financials suggests institutional investors are becoming more optimistic regarding credit conditions, business activity, and future earnings prospects.

- Importantly, the rally in Financials occurred alongside gains in Technology and Industrials, creating a more balanced market structure than has been evident during many recent advances.

Defensive Sectors Remain Well Supported

- One of the most notable characteristics of the session was the continued strength across defensive sectors. Utilities (XLU), Real Estate (XLRE), and Consumer Staples (XLP) all posted meaningful gains despite improving appetite for cyclical exposure.

- This dynamic suggests investors are not abandoning risk management in pursuit of growth. Instead, institutional portfolios appear to be maintaining diversified exposure across both offensive and defensive areas of the market.

- Such broad participation is often viewed as a positive signal because it reflects confidence without excessive speculation.

Technology Maintains Constructive Momentum

- Information Technology (XLK) gained 0.87%, extending its positive momentum. Although the sector did not lead the market, its ability to participate in the rally reinforces its role as a key pillar of institutional positioning.

- The ongoing strength reflects continued investor enthusiasm surrounding artificial intelligence, cloud infrastructure, and digital transformation themes. Technology remains one of the market's primary leadership groups despite increasing participation from cyclical sectors.

Communication Services and Health Care Lag

- Communication Services (XLC) and Health Care (XLV) were the only sectors to close lower during the session. However, the declines were relatively modest and do not suggest significant institutional distribution.

- Instead, the underperformance appears to reflect rotational activity as investors shifted capital toward sectors offering greater leverage to economic growth and commodity demand.

- The limited magnitude of the declines further highlights the constructive nature of the broader market environment.

Bottom Line

The June 12 session reflected one of the broadest sector advances seen in recent weeks. Materials (XLB) and Financials (XLF) emerged as the primary leadership groups, while Technology (XLK), Energy (XLE), Industrials (XLI), and Consumer Discretionary (XLY) also participated in the rally.

At the same time, continued gains in Utilities (XLU), Real Estate (XLRE), and Consumer Staples (XLP) demonstrate that investors remain committed to maintaining defensive exposure. This balanced participation across both cyclical and defensive sectors points to a healthy market backdrop characterized by improving confidence rather than excessive risk-taking.

Going forward, sustained leadership from Materials and Financials could strengthen the case for a broader market advance, particularly if Technology continues providing support and defensive sectors remain stable. The combination of cyclical strength and defensive resilience currently represents one of the most constructive sector configurations for the US equity market.

_06_12_2026_23_00_13_327450.jpg)

Please wait processing your request...

Please wait processing your request...