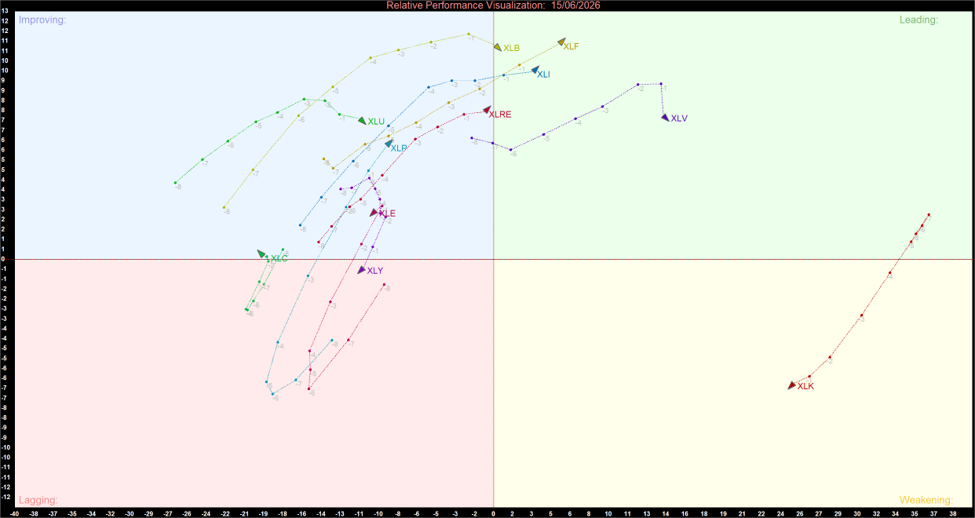

Key Highlights

- Materials Enters Leadership: Materials (XLB) has moved into the Leading quadrant, confirming strengthening relative strength and institutional support.

- Financials and Industrials Remain Strong: Financials (XLF) and Industrials (XLI) continue to lead, reflecting confidence in economic growth and cyclical sectors.

- Energy Continues Improving: Energy (XLE) remains in the Improving quadrant despite recent price weakness, indicating positive momentum development.

The US sector rotation profile remained constructive on June 15, 2026, with leadership broadening across multiple sectors. The latest Relative Rotation Graph (RRG) shows Financials, Industrials, Health Care, and Materials occupying the Leading quadrant, while several additional sectors continue to improve.

The transition of Materials into leadership and the ongoing improvement in Energy and Real Estate suggest healthy market breadth and continued institutional participation across both cyclical and defensive areas of the market.

US Sector Momentum Summary

US Sector Relative Momentum Chart (at the closing price of 15/06/2026). Powered by: amibroker.com

Key Market Themes

Leadership Expands Beyond Technology

- Financials (XLF), Industrials (XLI), Health Care (XLV), and Materials (XLB) now occupy the Leading quadrant. The presence of both cyclical and defensive sectors among market leaders reflects a balanced market environment and broad institutional participation.

- Materials' successful transition into Leading is particularly significant because it confirms strengthening relative strength after several weeks of improving momentum. The sector's advancement suggests increasing confidence in industrial activity, infrastructure spending, and commodity-linked industries.

Materials Establishes Itself as a New Leader

- Materials (XLB) represents one of the most important rotational developments on the chart. After spending several periods in the Improving quadrant, the sector has now crossed into Leading territory.

- This transition often reflects sustained institutional accumulation and growing investor conviction. The move also supports the broader theme of expanding leadership beyond Technology and into economically sensitive sectors.

Energy Shows Early Signs of Recovery

- Despite posting the weakest daily performance among all sectors, Energy (XLE) remains positioned in the Improving quadrant.

- The RRG highlights a key distinction between short-term price performance and longer-term relative momentum trends. While Energy continues to face near-term pressure, its improving momentum profile suggests that relative performance is beginning to stabilize.

- This development may indicate the early stages of a rotational recovery if positive momentum continues in the coming weeks.

Real Estate and Defensive Sectors Continue Improving

- Real Estate (XLRE), Utilities (XLU), Consumer Staples (XLP), and Communication Services (XLC) all remain in the Improving quadrant.

- The continued presence of multiple defensive sectors within Improving suggests that investors are maintaining diversified exposure rather than aggressively concentrating capital into high-risk growth areas.

- This broad participation supports a healthier market structure and reduces dependence on any single leadership group.

Technology Remains Strong Despite Momentum Cooling

- Technology (XLK) remains the only sector in the Weakening quadrant. However, its location far to the right of the benchmark continues to indicate superior relative strength versus the broader market.

- The sector's movement into Weakening should not necessarily be interpreted as bearish. Instead, it reflects a moderation in momentum following an extended period of leadership.

- Technology continues to serve as an important pillar of market strength, although leadership is increasingly being shared with Financials, Industrials, Materials, and Health Care.

Consumer Discretionary Remains the Primary Area of Weakness

- Consumer Discretionary (XLY) remains the only sector positioned in the Lagging quadrant.

- Although the sector generated a strong daily gain, relative strength remains below average and momentum has yet to fully recover. Continued improvement will be necessary before the sector can challenge for a position in the Improving quadrant.

Absence of Broad Weakness Supports Market Breadth

- One of the most constructive features of the current RRG structure is the concentration of sectors within either the Leading or Improving quadrants.

- With nine of the eleven sectors exhibiting positive momentum characteristics, institutional capital appears broadly distributed across the market. This pattern is generally associated with healthy market breadth and a more sustainable advance.

Bottom Line

The June 15 RRG configuration reflects a healthy and balanced market structure. Financials (XLF), Industrials (XLI), Health Care (XLV), and Materials (XLB) remain the primary leadership groups, while Energy (XLE), Real Estate (XLRE), Utilities (XLU), Consumer Staples (XLP), and Communication Services (XLC) continue to improve.

Although Technology (XLK) remains in the Weakening quadrant, its strong relative-strength position continues to support the broader market. Overall, the current sector rotation profile points to expanding leadership and constructive market breadth across US equities.

Please wait processing your request...

Please wait processing your request...