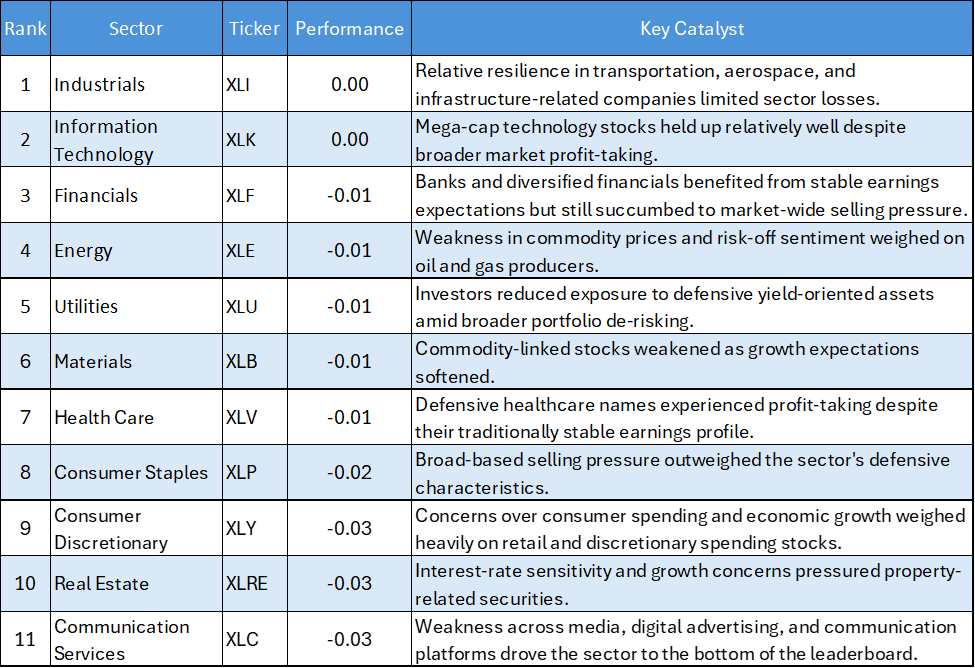

Key Highlights

- Industrials Prove Most Resilient: Industrials (XLI) declined just 0.14%, making it the best-performing sector during a broadly negative session and highlighting continued investor preference for economically sensitive businesses.

- Technology Holds Up Better Than the Market: Information Technology (XLK) fell 0.34%, significantly outperforming most sectors despite ongoing profit-taking across growth stocks.

- Consumer and Communication Sectors Lead the Sell-Off: Communication Services (XLC) plunged 2.78%, while Consumer Discretionary (XLY) and Real Estate (XLRE) each dropped 2.51%, making them the session's weakest performers.

- Defensive Sectors Fail to Provide Shelter: Consumer Staples (XLP), Health Care (XLV), and Utilities (XLU) all recorded losses exceeding 1.3%, indicating a broad-based risk-off environment rather than a simple rotation between growth and defensive sectors.

The US equity market delivered a widespread decline on June 17, 2026, with all eleven major S&P 500 sectors finishing in negative territory. Unlike previous sessions characterized by sector rotation, the latest trading day reflected broad-based risk reduction as investors trimmed exposure across both cyclical and defensive areas of the market.

The absence of any positive-performing sector suggests institutional investors adopted a cautious stance amid ongoing macroeconomic uncertainty. While Industrials and Technology demonstrated relative resilience, weakness across Communication Services, Consumer Discretionary, and Real Estate weighed heavily on overall market sentiment.

Daily US Sector Performance Summary

Key Market Themes

Broad-Based Risk-Off Sentiment Dominates

- The most notable feature of the session was the absence of any positive-performing sector. Such uniform weakness typically reflects a market-wide reduction in risk exposure rather than sector-specific developments.

- Institutional investors appeared more focused on capital preservation than sector rotation, resulting in simultaneous selling across growth, cyclical, and defensive segments of the market.

Industrials and Technology Display Relative Strength

- Although both sectors finished lower, Industrials (XLI) and Information Technology (XLK) significantly outperformed the broader market.

- The resilience of Industrials suggests investors continue to maintain confidence in long-term infrastructure spending, transportation demand, and industrial activity. Meanwhile, Technology's modest decline indicates institutional investors remain reluctant to aggressively reduce exposure to the market's primary growth engine.

Consumer Sectors Face Heavy Selling

- Consumer Discretionary (XLY) suffered one of the largest declines of the session, falling 2.51%, while Consumer Staples (XLP) dropped 2.23%.

- The simultaneous weakness in both discretionary and defensive consumer sectors suggests investors are becoming increasingly cautious about the broader consumer spending outlook. Rather than rotating from growth to safety, market participants reduced exposure across the entire consumer complex.

Real Estate Remains Under Pressure

- Real Estate (XLRE) matched Consumer Discretionary as the second-worst-performing sector. The decline highlights ongoing concerns regarding financing costs, property valuations, and the outlook for commercial real estate activity.

- The sector's underperformance suggests investors remain wary of interest-rate-sensitive assets despite recent moderation in bond market volatility.

Communication Services Becomes the Primary Laggard

- Communication Services (XLC) posted the largest decline among all sectors, falling 2.78%.

- The weakness points to selling pressure across digital advertising, media, streaming, and communication platform businesses. The move also reflects investor caution toward sectors that have delivered strong gains earlier in the year and may now be experiencing profit-taking activity.

Defensive Areas Fail to Provide Protection

- Utilities (XLU), Health Care (XLV), and Consumer Staples (XLP) all recorded substantial losses despite their defensive characteristics.

- This pattern suggests the session was driven by broad risk reduction rather than a rotation into traditionally defensive assets. When defensive sectors decline alongside growth sectors, it often reflects heightened market caution and widespread portfolio rebalancing.

Bottom Line

The June 17 session reflected a clear risk-off environment, with all eleven major US sectors closing lower. Industrials (XLI), Technology (XLK), and Financials (XLF) demonstrated the strongest relative resilience, while Communication Services (XLC), Consumer Discretionary (XLY), and Real Estate (XLRE) absorbed the heaviest selling pressure.

The broad-based nature of the decline suggests investors were reducing overall market exposure rather than rotating between sectors. Going forward, market participants will be watching whether the relative strength displayed by Industrials and Technology evolves into renewed leadership or whether weakness spreads more evenly across the market.

Please wait processing your request...

Please wait processing your request...