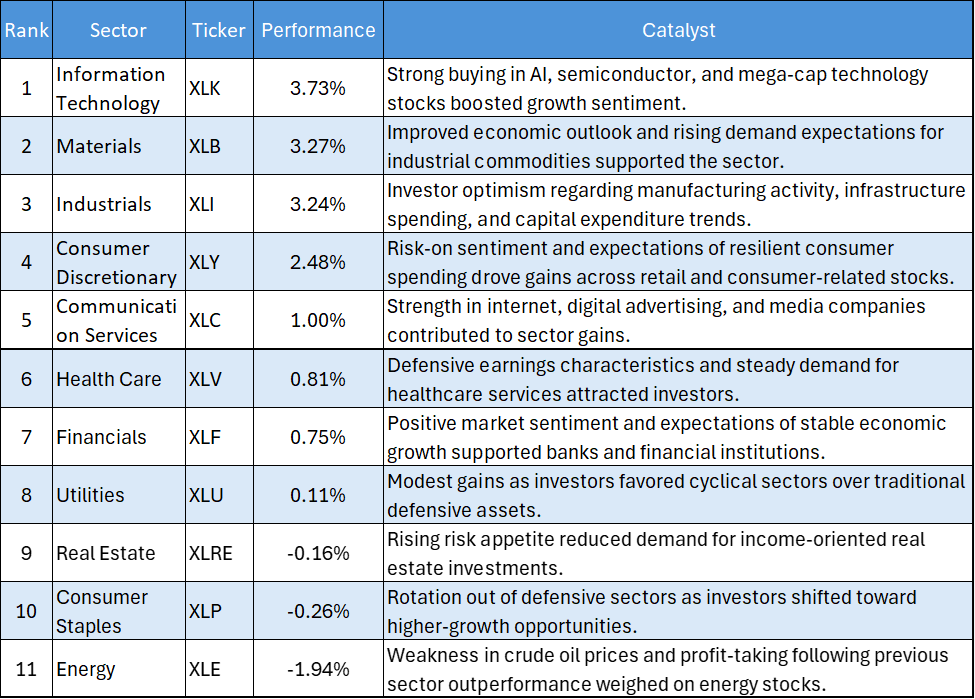

Key Highlights

- Technology Reclaims Market Leadership: Information Technology (XLK) surged 3.73%, making it the strongest-performing sector of the session. The sharp advance signals renewed investor confidence in growth-oriented equities and highlights strong demand for technology-related stocks.

- Materials and Industrials Follow Closely: Materials (XLB) gained 3.27%, while Industrials (XLI) advanced 3.24%, reflecting improving risk sentiment and growing optimism toward economically sensitive sectors. The broad participation suggests investors are positioning for stronger economic activity.

- Consumer Discretionary Benefits from Risk-On Rotation: Consumer Discretionary (XLY) rose 2.48%, supported by renewed buying interest across higher-beta consumer names. The strong performance indicates increasing confidence in consumer spending and economic resilience.

- Energy Emerges as the Sole Major Laggard: Energy (XLE) declined 1.94%, making it the weakest-performing sector of the session. The underperformance contrasts sharply with gains elsewhere and suggests investors are rotating away from commodity-linked assets in favor of growth opportunities.

The US equity market delivered a powerful rally on June 11, 2026, with nearly every major sector closing in positive territory. Unlike recent sessions characterized by defensive positioning, investors aggressively rotated into growth and cyclical industries, fueling broad-based gains across the market.

Technology, Materials, Industrials, and Consumer Discretionary sectors led the advance, while traditionally defensive sectors posted more modest gains. The session reflected a significant improvement in market sentiment as investors increased exposure to sectors most closely tied to economic growth and corporate earnings expansion.

Daily US Sector Performance Summary

Key Market Themes

Growth Stocks Return to Favor

- Information Technology (XLK) led all sectors with a gain of 3.73%, marking a decisive return of investor appetite for growth-oriented equities. The strong rally suggests institutional investors are once again willing to allocate capital toward sectors with higher earnings growth potential.

- The leadership from Technology was accompanied by gains in Communication Services (XLC) and Consumer Discretionary (XLY), indicating broad-based strength across growth-related industries rather than isolated sector-specific buying.

Cyclical Sectors Participate Aggressively

- Materials (XLB) and Industrials (XLI) both posted gains exceeding 3%, highlighting strong investor confidence in sectors that typically benefit from economic expansion. Such performance often reflects improving expectations for manufacturing activity, infrastructure spending, and industrial demand.

- The synchronized rally across cyclical industries points to a constructive outlook for economic growth and corporate profitability in the near term.

Defensive Sectors Lag Behind

- Traditional defensive sectors delivered comparatively muted performance. Utilities (XLU) gained only 0.11%, while Consumer Staples (XLP) declined 0.26%.

- The relative weakness of defensive industries suggests investors are reducing capital allocations to lower-volatility assets and embracing a more aggressive risk posture.

Financials and Health Care Provide Additional Support

- Financials (XLF) advanced 0.75%, while Health Care (XLV) rose 0.81%, contributing to the broad participation observed throughout the market.

- Although these gains were smaller than those seen in Technology and Industrials, they reinforce the notion that buying activity was widespread rather than concentrated in a handful of sectors.

Energy Faces Profit-Taking Pressure

- Energy (XLE) was the only sector to record a significant decline, falling 1.94%. The weakness suggests investors may be rotating capital away from commodity-linked assets after previous outperformance.

- The sector's divergence from the broader market highlights a shift in leadership toward growth and economically sensitive industries rather than resource-based investments.

Bottom Line

The June 11 session showcased a strong risk-on environment across US equity markets. Information Technology (XLK), Materials (XLB), Industrials (XLI), and Consumer Discretionary (XLY) emerged as the clear leaders, reflecting improving investor confidence and growing optimism regarding economic growth prospects.

Meanwhile, traditionally defensive sectors such as Consumer Staples (XLP), Utilities (XLU), and Real Estate (XLRE) lagged the broader market, indicating a notable shift away from capital preservation strategies. Energy (XLE) stood out as the lone major underperformer amid widespread buying elsewhere.

Going forward, continued leadership from Technology and cyclical sectors would reinforce the bullish market backdrop, while sustained weakness in defensive sectors may further signal that investors remain focused on growth opportunities rather than downside protection.

Please wait processing your request...

Please wait processing your request...