When the purchasing power of currency erodes, tangible assets with intrinsic value have historically preserved — and often grown — wealth. Here is everything you need to know about hard assets as an inflation hedge.

What are hard assets?

Hard assets are tangible, physical resources with intrinsic value — meaning their worth exists independent of any government guarantee or counterparty promise. Unlike stocks, bonds, or cash, hard assets cannot be inflated away to zero because they represent real, physical things the world needs: shelter, food, energy, and industrial inputs.

The major categories include:

Source: Kalkine

The rationale: why do hard assets thrive in high inflation?

Inflation reduces the real purchasing power of money. When $1 buys less tomorrow than it does today, assets with real-world utility and limited supply naturally appreciate in nominal terms. There are several interconnected mechanisms at work:

1. Supply constraints meet rising replacement costs

Physical assets cannot be created with a keystroke. Building a new office tower, extracting gold from a mine, or cultivating farmland all require significant time and capital. When inflation raises the cost of labor, materials, and energy, the replacement cost of existing assets rises — pulling their market value upward.

2. Revenue and rents adjust upward

Many hard assets generate income that escalates with inflation. Commercial real estate leases often include CPI escalators. Commodity producers charge more as input costs rise. Infrastructure assets (pipelines, toll roads) frequently have regulated rates tied directly to inflation indices.

3. Currency debasement boosts relative value

When central banks expand the money supply to combat economic downturns — a common policy that can feed inflation — the value of paper currency falls relative to scarce physical assets. Gold, in particular, has served as a monetary alternative for thousands of years, maintaining purchasing power across centuries.

4. Demand inelasticity

Core commodities like oil, copper, and agricultural products have inelastic demand — people continue to need energy, construction materials, and food regardless of price. This demand floor supports prices even during economic slowdowns.

Data Source: EODHD/Others, Analysis by Kalkine

Key hard asset classes examined

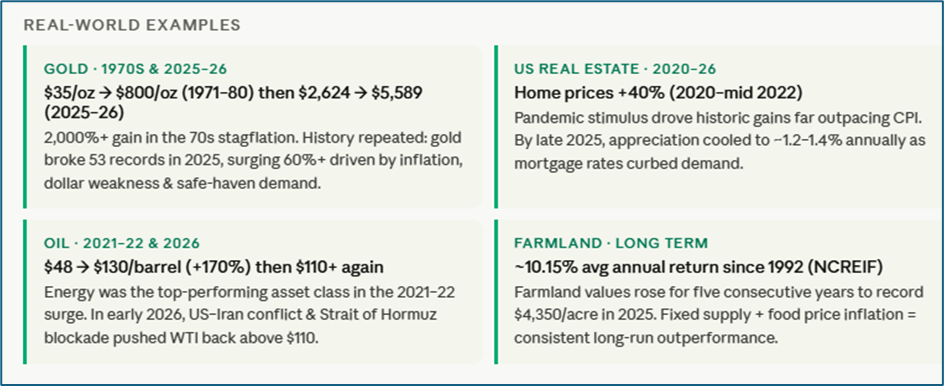

Real estate: Real estate is widely regarded as one of the most reliable inflation hedges. Property owners benefit on two fronts simultaneously: the nominal value of the asset rises with inflation, while rental income — the asset's cash flow — also tends to increase as landlords pass higher costs to tenants. Leverage (mortgages) amplifies returns since the debt is repaid in cheaper future dollars.

Real Estate Investment Trusts (REITs) offer a liquid, publicly traded alternative. Certain REIT subcategories — industrial, self-storage, and residential — have historically shown strong inflation beta.

Gold and precious metals: Gold is the archetypal inflation hedge. It has no counterparty risk, cannot be printed, and is universally recognized as a store of value. Its correlation with the US dollar is historically negative: when the dollar weakens (often a byproduct of inflationary policies), gold prices tend to rise. Silver has a similar dynamic but with greater industrial demand exposure, making it more volatile.

Central banks globally purchased 863 tonnes of gold in 2025 (World Gold Council), bringing estimated global official gold reserves to approximately 36,359 tonnes as of September 2025 — up from ~35,000 tonnes cited in 2024 editions. Despite a 21% dip from the record 1,000+ tonne annual pace of 2022–2024, the 2025 figure still ran well above the pre-2022 historical average of 400–500 tonnes per year. Gold also overtook US Treasuries in late 2025 to become the world's largest reserve asset by value.

Oil and energy: Energy prices are a direct input into the Consumer Price Index calculation. When oil and gas prices rise, inflation measures follow. Investing in energy commodities or producers therefore offers a direct hedge against the very index investors are trying to beat. Integrated oil companies also benefit from rising refinery margins and exploration asset values.

Copper and industrial metals: Copper is often called "Dr. Copper" for its ability to signal economic health. In inflationary environments driven by supply constraints or strong demand, industrial metals tend to perform well. Copper is also central to the global energy transition — electric vehicles and grid infrastructure require significantly more copper than their fossil-fuel equivalents — adding a structural demand tailwind.

Agricultural commodities: Food inflation tends to be one of the most visible and politically sensitive components of overall CPI. Agricultural commodities — corn, wheat, soybeans, livestock — directly benefit when input costs and food prices rise. Farmland investment takes this a step further by capturing both the commodity price upside and the land appreciation.

Hard assets vs. financial assets in inflationary periods

Financial assets — stocks and bonds — have a more complex relationship with inflation. Fixed-rate bonds lose real value when inflation rises, since coupon payments become worth less in real terms. Equities are mixed: companies with pricing power can pass inflation to customers (supporting earnings), while those with high debt or thin margins may be hurt by rising rates and costs.

The Bloomberg Commodity Index and GSCI Commodity Index have both demonstrated that commodity baskets outperformed both the S&P 500 and US Treasuries during the high-inflation periods of the 1970s and the 2021–2022 cycle.

Risks and limitations

Hard assets are not without risks. Real estate is illiquid and management-intensive. Commodity prices are volatile and can fall sharply when demand slows. Gold generates no income, meaning investors sacrifice yield. Infrastructure requires large upfront capital. Additionally, hard assets can underperform significantly during deflationary periods or economic contractions when demand collapses.

Leverage in real estate can also amplify losses in downturns, as the 2008 financial crisis demonstrated. Diversification across multiple hard asset classes — rather than concentration in one — is widely considered a more resilient strategy.

Future outlook

Several structural trends suggest hard assets will remain a strategically relevant allocation in the years ahead:

Energy transition demand: The global shift toward renewable energy requires vast quantities of copper, lithium, cobalt, nickel, and rare earth elements. The International Energy Agency (IEA) projects that a net-zero energy system by 2050 would require six times more mineral inputs than today, creating a potential multi-decade demand supercycle for industrial metals.

Deglobalization and supply chain reshoring: Post-pandemic and geopolitical tensions are driving countries to reshore manufacturing and diversify supply chains. This raises the cost of goods, supports commodity prices, and increases demand for industrial real estate (warehouses, manufacturing facilities).

Fiscal policy and debt levels: Government debt levels in major economies reached historic highs following pandemic-era spending. Historically, high debt loads have been associated with eventual inflation or currency debasement — conditions favorable to hard asset ownership.

Global food security: Climate variability, geopolitical conflict (particularly in key agricultural regions), and growing middle-class food demand in emerging markets are creating persistent upward pressure on agricultural commodity prices and farmland values.

That said, the trajectory of central bank policy — particularly whether rate hikes successfully contain inflation — will significantly influence the near-term performance of hard assets. A sustained deflationary environment or deep recession could compress commodity prices even as structural demand trends remain intact over the longer term.

Bottom line

Hard assets have a well-documented historical track record of preserving purchasing power during inflationary periods. While no single asset guarantees protection in every environment, a diversified allocation across real estate, precious metals, energy, and industrial commodities provides a meaningful buffer against currency debasement and rising prices. As of April 2026, gold's historic rally to above $5,500/oz, resurgent energy prices tied to the US–Iran conflict, and a renewed uptick in CPI to 3.3% (March 2026) offer a live illustration of these dynamics at work. Understanding the mechanisms — replacement cost, rental escalation, supply inelasticity, and dollar hedging — helps investors make informed, rational decisions rather than reactionary ones.

Please wait processing your request...

Please wait processing your request...