Despite surging oil prices and the US blockade of the Strait of Hormuz, equity markets remain surprisingly calm. Analysts say peak fear has passed. Here is what the data actually signals.

The Anatomy of a Calmer Panic

There is a particular kind of market behaviour that emerges after the initial shock of a geopolitical rupture has been absorbed. Sell orders slow. Volatility indicators plateau. Traders stop reacting to every headline and begin, instead, to assign probabilities. That transition appears to be underway across global capital markets following the US decision to blockade the Strait of Hormuz.

Asian equity benchmarks fell roughly 1% on Monday. US futures followed in similar modest fashion. These are not the movements of a market in freefall. They are the movements of one recalibrating.

The contrast with earlier stages of the US-Iran conflict is instructive. When hostilities first escalated, implied volatility spiked, institutional portfolios repositioned defensively, and cross-asset correlations tightened in the classic risk-off pattern. That phase, most analysts now believe, has passed. The VIX, having peaked in the early weeks of the conflict, has since retreated; what some strategists are now calling the high-water mark of fear. The risk premium was front-loaded. The shock has been priced.

Underlying this shift is a growing conviction among investors that the escalation is, at least in part, a function of negotiating posture rather than strategic inevitability. Several market participants have characterised the administration's moves as tactical brinkmanship, suggesting that the endpoints of the conflict are more bounded than the headlines imply. As sentiment among investment strategists reflects, markets now have a better understanding of the motivations at play and are pricing accordingly. The reaction function, in other words, has become less reflexive.

What remains is the second-order question: not whether markets feared, but what they now expect.

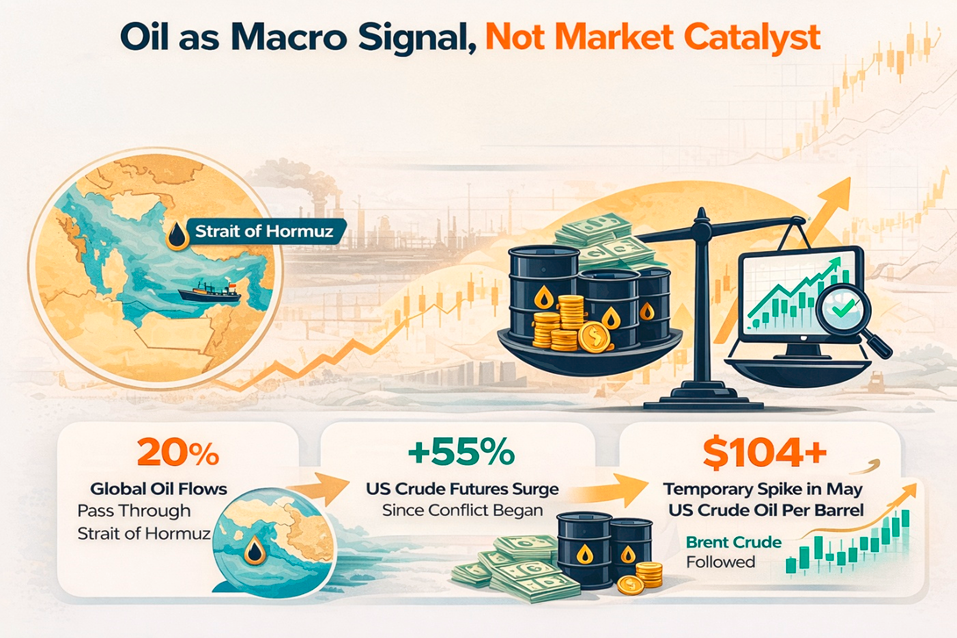

The Strait of Hormuz handles approximately one-fifth of global oil flows. Its disruption carries structural weight. US crude oil futures have surged more than 55% since the conflict began, with May delivery contracts briefly trading above $104 per barrel. Brent crude followed closely.

And yet equities have not collapsed.

This divergence is analytically significant. When oil shocks coincide with equity sell-offs of similar magnitude, markets are pricing broad economic damage: demand destruction, earnings compression, recessionary pressure. When oil surges while equities hold relatively firm, the implied reading is different. Markets are treating the energy shock as an inflation event, one that tightens monetary conditions and compresses multiples at the margin, but does not fundamentally alter the earnings outlook.

That distinction shapes everything that follows. Higher oil feeds into inflation expectations, which delay rate cuts, push bond yields higher, and strengthen the dollar. The 10-year Treasury yield has risen sharply since the conflict began. The dollar index has gained ground. These are the transmission mechanisms of an energy shock, and they are functioning as expected.

What is not functioning as expected is gold.

Gold's Anomalous Retreat

In standard geopolitical risk frameworks, gold appreciates when uncertainty rises. Investors seek non-sovereign stores of value. Bullion becomes a hedge against systemic disruption.

That has not happened here. Spot gold has declined even as Hormuz tensions have escalated. The explanation most commonly offered is that emerging market central banks have been selling reserves to defend their currencies against a strengthening dollar. Liquidity needs, in other words, are trumping fear.

This matters beyond gold itself. It suggests that the current market regime is not one of deep systemic fear, but of liquidity management and real-rate repricing. Investors are not fleeing to safety so much as they are rotating toward yield and cash equivalents in response to a macro environment that has shifted.

That is a fundamentally different regime from the one that typically precedes a sustained equity bear market.

The Political Clock Markets May Be Ignoring

There is one variable that analysts have flagged as meaningfully underpriced: the domestic political constraint on the US executive.

War powers legislation gives the administration a limited window to conduct military operations without explicit congressional authorisation. That window is not indefinite. Lawmakers are reportedly preparing resolutions to require congressional approval for any further military action against Iran. The pressure to either escalate decisively or pursue a negotiated off-ramp is therefore not merely strategic; it is constitutional.

This introduces what might be called duration risk: the possibility that the conflict persists longer than markets currently expect, or that the political resolution takes a more disruptive form than the orderly de-escalation being priced in. If the administration is forced into a corner by congressional pressure, the outcome space becomes less predictable, not more.

Markets are currently assigning high probability to a negotiated resolution. Whether that probability is well-calibrated remains to be seen.

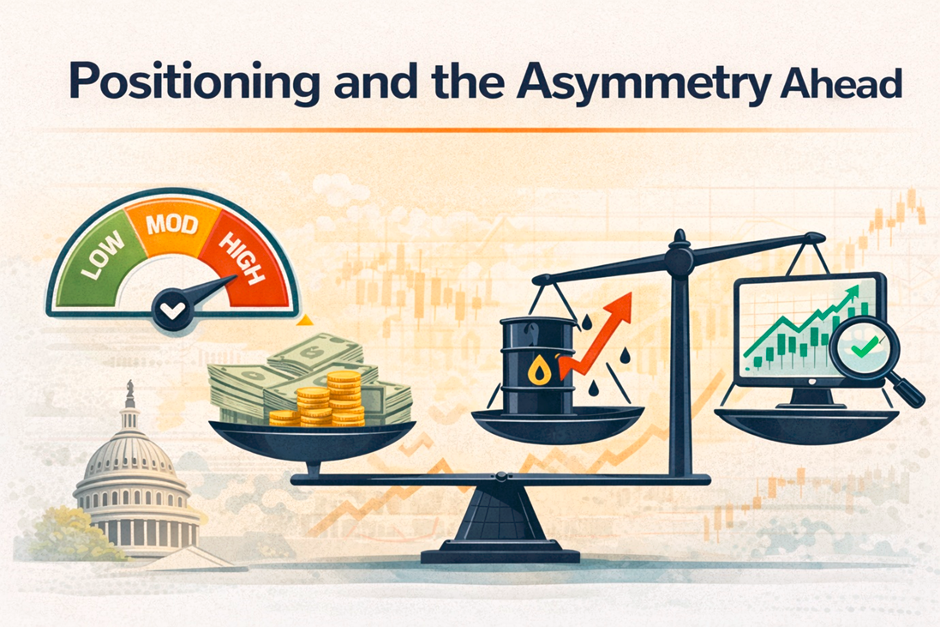

Institutional portfolios, by most accounts, remain defensively positioned. Elevated cash holdings, hedges against further equity declines, and underweights in cyclical sectors suggest that the capitulation point has not yet been reached. There has been caution, not panic.

This creates a particular kind of asymmetry. If the conflict de-escalates on the trajectory markets currently expect, and if the negotiation-tactics reading of the administration's posture proves correct, positioning is too defensive and equities have room to recover. If the conflict deepens materially, or if the oil shock proves more persistent than anticipated, portfolios have not yet fully priced the downside.

The range of outcomes has narrowed from the binary logic of early conflict pricing, but the distribution has not yet collapsed into certainty. Markets are operating in a grey zone: pricing partial outcomes, discounting temporary disruptions, and reserving judgement on scenarios that have not yet materialised. Volatility has eased compared to the early weeks of the conflict, and the mood among portfolio managers has shifted from reactive to interpretive, from selling on headlines to working through what the situation ultimately means.

That is a more sophisticated and arguably more fragile equilibrium than it first appears. It depends heavily on the assumption that disruption is temporary. Should oil supply constraints persist beyond the near term, or should congressional friction delay the administration's ability to negotiate, the inflation feedback loop currently priced as transitory could begin to look structural.

At that point, the calm that has settled over equity markets would face a more serious test.

Please wait processing your request...

Please wait processing your request...